From the supply side, due to the significant drop in raw material costs in the early stage, the profits of some finished materials have improved, and the enthusiasm for resuming production at some steel mills has notably increased, which will bring new pressures to the supply side later on. From the demand side, under the influence of the "buy high, not low" mindset, there has been some release of inventory demand. However, as steel prices continue to rebound, the enthusiasm for hoarding among some traders has begun to wane, and market transaction volumes have also gradually decreased. Whether the terminal demand will be released as scheduled has become a focal point of the market. From the cost side, as the enthusiasm for resuming production at some steel mills continues to grow, the procurement demand for raw materials has also expanded, driving the resurgence of iron ore and scrap steel prices. Meanwhile, coking coal prices have shifted from a decline to an upward game. In the short term, the domestic steel market will face the situation of steel mills actively preparing for resumption of production, decreasing enthusiasm for production and inventory, pending release of terminal demand, and a shift from weak cost support to strong support. According to the weekly price prediction model data of the Lang Steel Cloud Commerce Platform, the domestic steel market is expected to see a slight upward trend with fluctuations next week (Aug. 8-12, 2022), but there is a possibility of steel prices reversing due to insufficient demand release as expected.

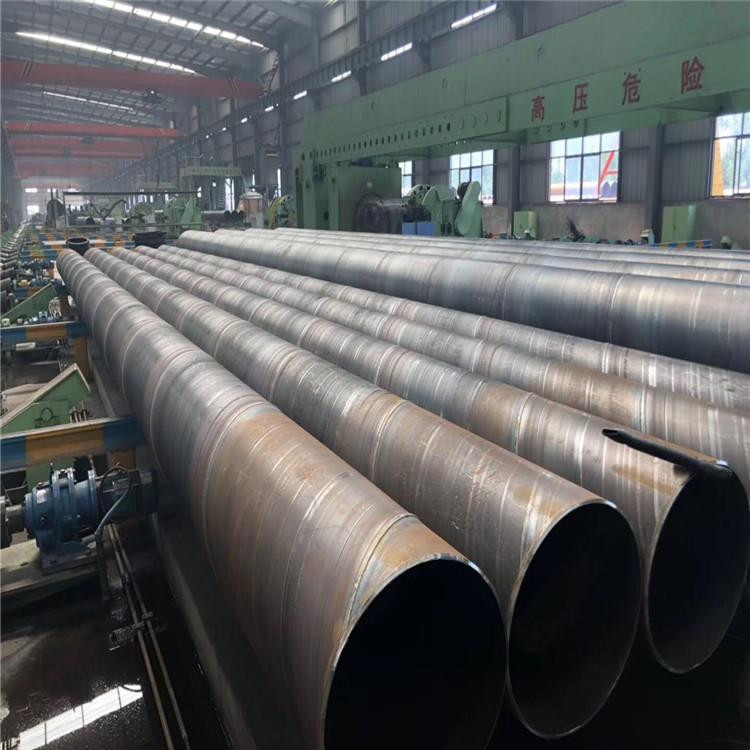

On August 3rd, the domestic welded pipe galvanized pipe prices remained stable with a slight upward trend. According to the monitoring data from the Langang Iron and Steel Cloud Merchant Platform: The average price of 4-inch (3.75mm) welded pipes in domestic cities was 4450 yuan, with all central city quotations unchanged from the previous day; The average price of 4-inch (3.75mm) galvanized pipes in domestic cities was 5313 yuan, up 3 yuan from the previous day. Among the central cities, prices in Tianjin rose by 30 yuan, while other cities remained unchanged from the previous day.

Today, the factory exit prices of most steel mills in North China and Northwest China have increased by 30-50 yuan, but the actual shipment changes are minimal. Taking Tangshan as an example, the current factory price for 4-inch welded pipes in Tangshan is around 4070 yuan, and for galvanized pipes, it's around 4920 yuan. The futures market has seen volatility and upward movement today, with raw material prices boosting market sentiment. However, the recent* situation changes rapidly, leading to cautious market operations and overall average transactions. In terms of the market, most areas lack the momentum to follow the rise, and today's market is mainly stable. It is understood that after the price increase, steel traders' transactions have not significantly improved compared to July. Recent mixed messages of supply and demand have affected trading atmosphere, and the hot and humid weather has also impacted the market's trading rhythm. Overall, with costs rising gradually, and as we enter August, seasonal factors are becoming less influential, market sentiment is slightly recovering. In the short term, the prices of welding pipes are expected to see limited fluctuations and mainly stabilize.