Construction Project Tracking Audit refers to the process in which independent auditing institutions and auditors, including social intermediary organizations and professionals assisting the auditing department, utilize auditing techniques to review, supervise, analyze, and evaluate the authenticity, legality, and efficiency of economic management activities at all stages of a construction project, from investment and approval to completion and delivery for use, in accordance with the relevant national laws, regulations, and institutional norms.

The aim is to effectively control and accurately reflect the construction cost, safeguard legitimate rights and interests, improve project management, and enhance investment returns.

Project construction tracking audits are divided into pre-construction audits, construction period audits, completion settlement audits, and financial closing audits.

Pre-start Audit refers to an audit of the legality and compliance of project procedures, as well as the authenticity and rationality of the investment estimate. It mainly includes the following contents:

(1) Annual Construction Plan and Project Progress Schedule.

(2) Expand the basis for preliminary design, the justification of design proposals, the preparation of the general estimate, and the approval process.

(3) Planning and permit approval procedures.

(4) Source of Construction Funds and Implementation Status

(5) Construction drawing design area, decoration standards, and approval status by relevant departments.

(6) Bidding and tender procedures, content of bid documents, and procedures for compiling the bid benchmark.

(7) Bid Project Bottom Price and Quantity Pricing List.

(8) Status of Construction Contract Establishment.

(9) Status of implementation for construction site and necessary utilities such as water, electricity, and road access.

(10) Other circumstances related to the project approval for construction.

Audit During Folding Construction

Construction Period Audit refers to the audit department's review of matters such as project management, construction progress, project materials, and change negotiations during the construction period. It mainly includes the following contents:

Establishment and implementation of internal control systems.

(2) Construction timeline, progress, and funding/materials availability. Project tracking and audit (3) As-built record of concealed works, monthly progress reports.

(4) Management of equipment and material procurement, storage, and usage.

(5) Negotiation on design, technology, and material changes.

(6) Other circumstances related to management during the construction period.

Collapsible Completion and Settlement Audit

Completion audit refers to the audit department's review of the cost of various construction projects after completion. It mainly includes the following contents:

(1) Basis for the preparation of engineering settlement.

(2) Quantity of work and usage, pricing of main materials, labor costs, material expenses, equipment usage fees, and定额application.

(3) Comprehensive fee bases, rates, and other related matters.

(4) Execution of the bidding project's bid bottom and cost estimate of work quantities.

(5) Construction payment to contractors and control over material and equipment pricing.

(6) Other circumstances related to the project completion and settlement.

Collapsible Financial Year-End Audit

Financial closing audit refers to the audit of the investment confirmation for the entire construction project by the auditing department. It mainly includes the following contents:

(1) Approved design plans and actual completion status of the engineering.

(2) Completion of acceptance inspection and handling of remaining issues.

(3) Completion amount of investment in construction and installation projects, equipment investment, deferred investment, and other investments, as well as the transfer status of assets put into use.

(4) The authenticity, compliance, and completeness of the final accounts statement.

Function

Enhance and improve the management level of construction entities

Lack of management expertise among the main bodies of construction project management often leads to the adoption of traditional, experience-based administrative models. Frequent mismanagement decisions result in economic losses. On one hand, management is continuously under control; on the other hand, the responsibilities of stakeholders are unclear, leading to disjointed operations, causing chaos in the intrinsic organic connections of construction projects. This results in a lack of coordination among relevant units during the construction process and a low level of management. Through continuous auditing, work can be carried out in financial management and inter-coordination, which can promote the improvement of the management level of the main bodies of construction project management.

Promote the fulfillment of duties by all supervisors, ensuring the completion of their respective tasks.

The construction unit relies on the supervisory agency for project management and supervision, while the supervisory agency focuses on engineering quality and progress management, seldom considering aspects such as project cost, accounting, financial control, and material procurement. This leads to improper handling of project implementation and final settlement, leaving unresolved conflicts and management regrets. The construction unit ends up paying for lessons learned without any further action. The result is a loss for both the country and the owner. Through follow-up audits, better control over cost estimation and management can be achieved, and timely corrections and accountability for errors caused by supervisory agencies and other relevant departments can be pursued. Thirdly, follow-up audits can promote a shift in the concept of engineering audits. The current audit of construction projects often falls into the "nine heavy and nine light" mindset, which emphasizes budgeting and settlement over early planning and decision-making, as well as post-construction decision-making and evaluation. It prioritizes construction fund audits over management activity supervision, static post-event supervision over dynamic process control, compliance over the authenticity and effectiveness of audit items, traditional audit methods over innovative modern audit theories, internal audit procedures over external influences, local issue handling over philosophical considerations of audit development, theoretical derivation over the combination of audit theory and practice, and the inability of audit positioning to participate in management processes and provide decision-making opinions, over the role of engineering audit in management and supervision.

Due to the varying perceptions or consensus among most people, including auditors, regarding the involvement of audits in construction projects, many believe that being on-site and involved in management constitutes overstepping boundaries. Many think auditors cannot act as both judges and players. According to Article 22 of the "Audit Law," which states that "audit authorities shall supervise the implementation of budgetary expenditures and the final accounts of completed construction projects" [1], this necessitates that the audit's involvement in the process is not considered an overstep but rather an acknowledgment that for years, the audit of construction projects has not been thorough enough, and the true functions of audit supervision and evaluation have not been fully carried out.

By tracing audits, promote the standardization of the bidding and tendering market

Following the promulgation of the National Tendering and Bidding Law, China's construction tendering and bidding market has preliminarily matured in cultivation and development. However, due to various reasons, there are still phenomena such as clandestine operations in tendering and bidding, non-public "open bidding," arbitrary modification of bidding methods, collusive bidding, and other irregularities that even seriously violate the Tendering and Bidding Law. Through tracking audits, it can standardize the management behaviors of construction units, prevent malpractice and corruption from the source, control engineering cost, reduce project costs, and improve the efficiency of national investment, all of which will play a positive role.

Construction project tracking audit, as an innovative approach to engineering audit, has already demonstrated its effectiveness in practice.

Shanghai Zhida Engineering Consulting Co., Ltd. was established in 1996 and is affiliated with Shanghai Hanzhi Construction Group Co., Ltd. It holds a Class-A qualification in cost consultation issued by the Ministry of Housing and Urban-Rural Development. We are capable of undertaking comprehensive services such as cost consultation, project management, and full-process consultation for various construction and municipal engineering projects across the country.

The company boasts a high-quality management team with extensive experience in construction and civil engineering, currently comprising 186 cost professionals, including over 46 state-registered cost engineers and registered consulting engineers, as well as more than 50 other technical specialists. The company has an advisory group of renowned experts in urban roads, civil engineering, and other fields, providing robust technical support for resolving technical difficulties in the management of our engineering projects.

Cost Estimate Class-A Qualification

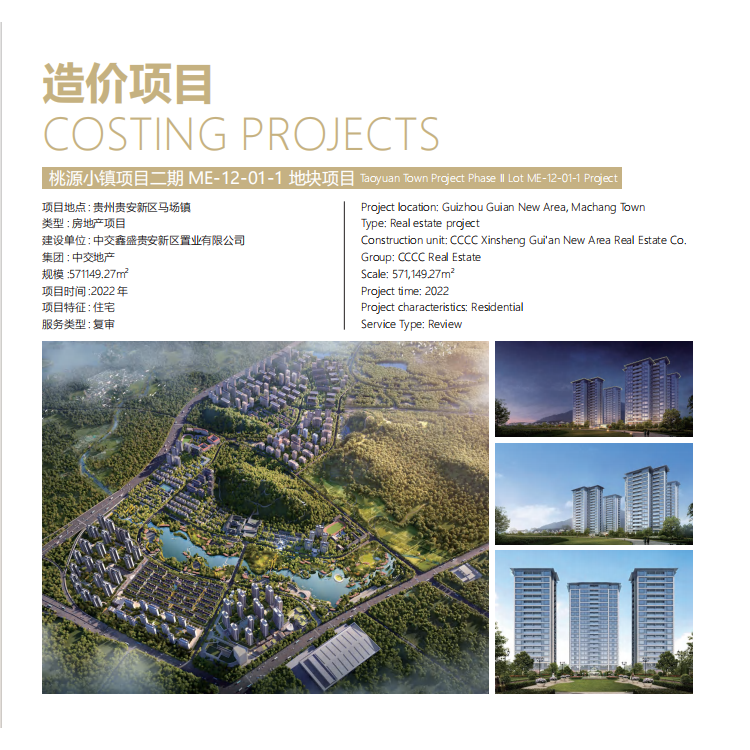

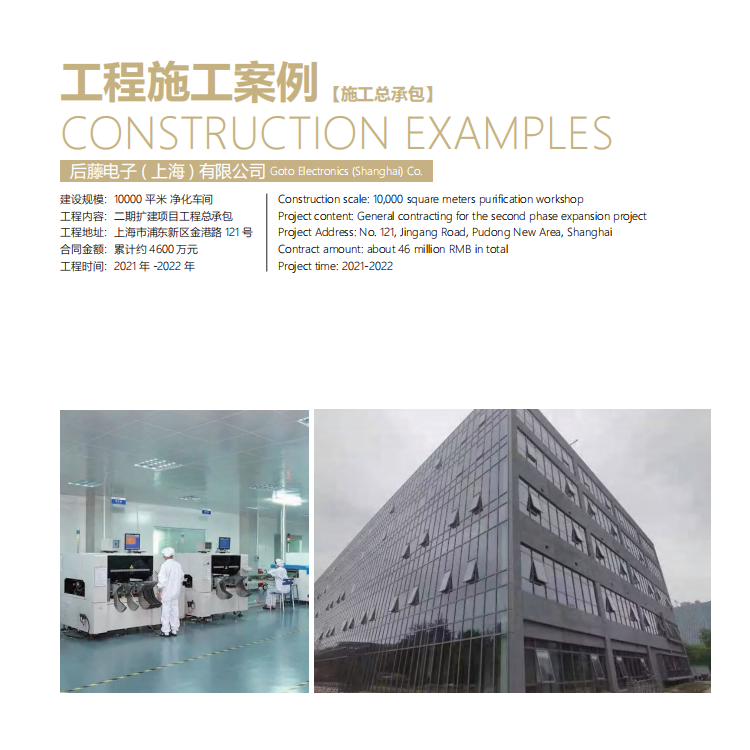

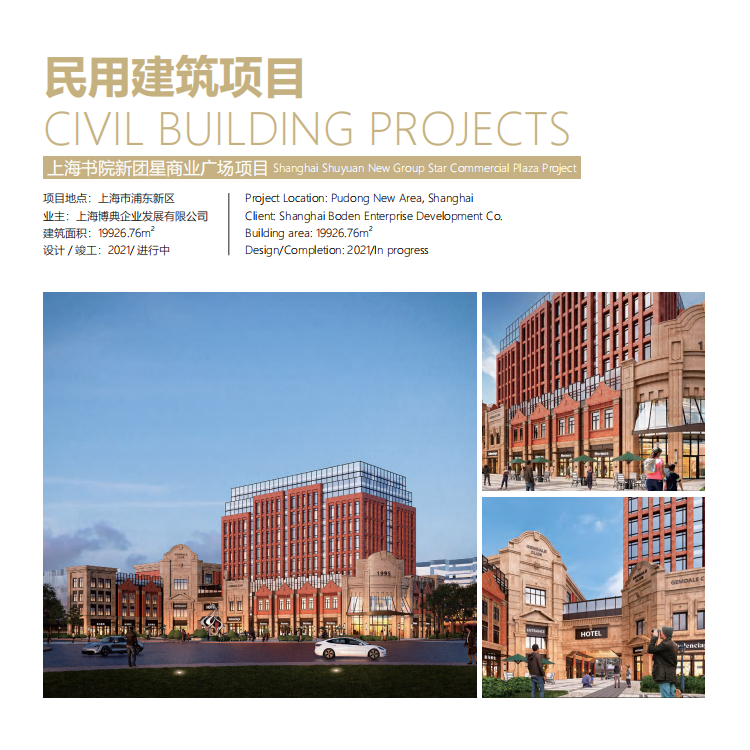

Success Stories: