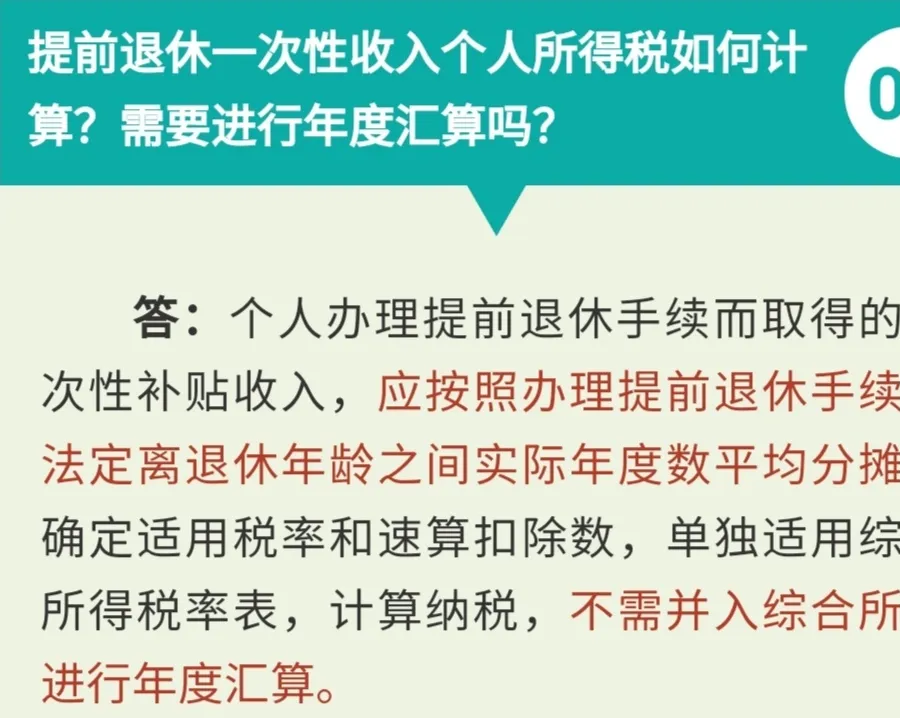

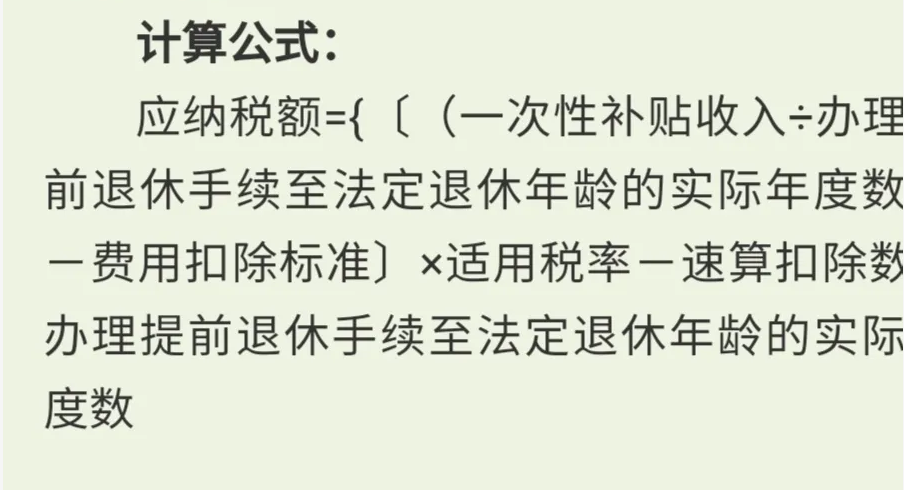

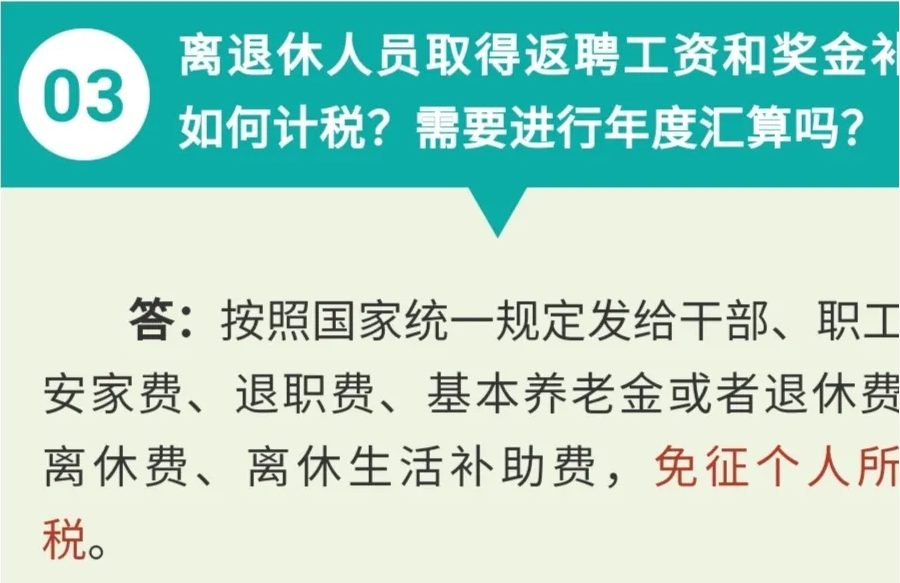

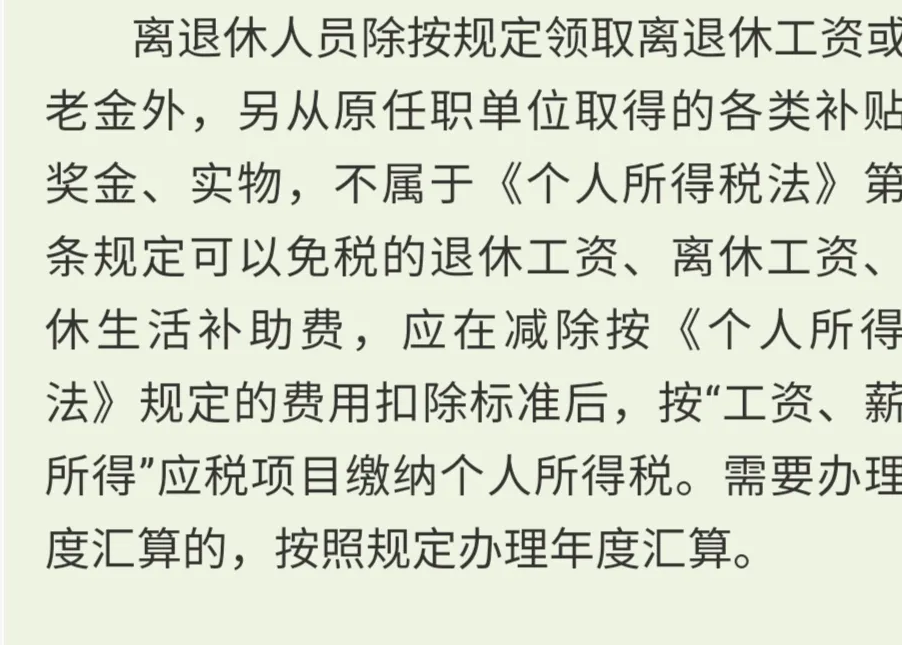

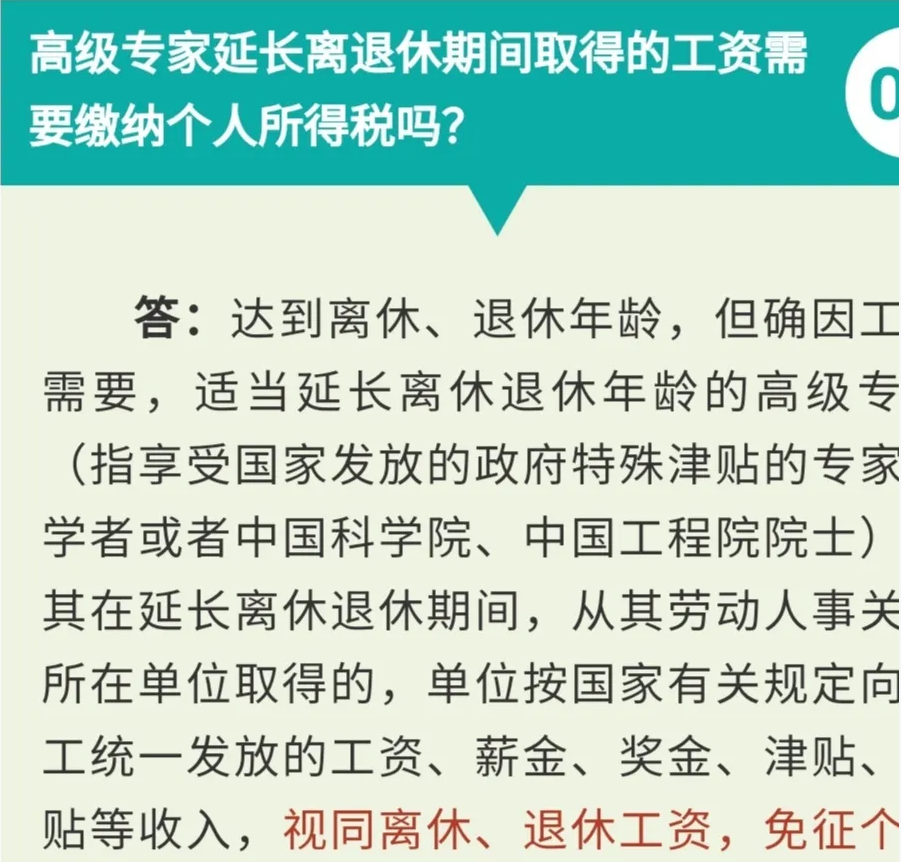

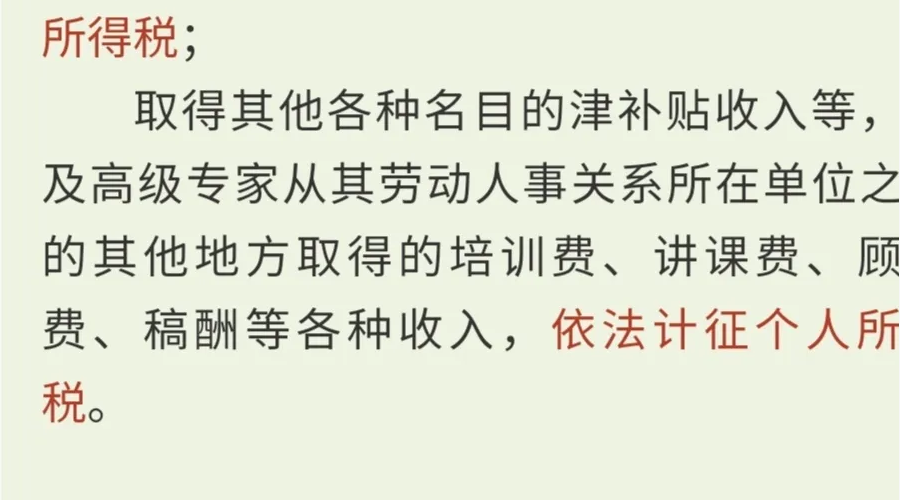

Previously, Shen Shui Xiaowei provided you with popular Q&A regarding salary and wages in the individual income tax settlement. Today, in response to your high关注度 questions, we have compiled nine Q&A on salary and wages to further help you understand the relevant policies. Let's take a look together.

How is personal income tax calculated for the withdrawal of corporate annuity and professional annuity? Do they require annual tax reconciliation?06

Answer:Upon reaching the national retirement age, individuals are entitled to receive the corporate annuity and professional annuity as stipulated by regulations.Not included in the comprehensive income for annual settlementFull amount to be calculated separately for taxable liabilities.Monthly distributions are taxed based on the monthly tax rate schedule; quarterly distributions are prorated and included in each month, taxed at the monthly rate based on the average quarterly amount; annual distributions are taxed using the comprehensive income tax rate schedule.

07How to Calculate Personal Income Tax on Deferred Tax-Deferred Commercial Annuity Payments? Do They Require an Annual Tax Reconciliation?

Answer:Individuals receive pension income from tax-deferred commercial annuity insurance as stipulated by regulations.25% of the amount is exempt from tax, with the remaining 75% subject to a personal income tax rate of 10%.After being deducted and paid by the insurance agency, a full-member, full-amount deduction and declaration is processed at the institution where the individual purchases the tax-deferred pension insurance.No need to include in the comprehensive income for annual settlement.

What conditions must be met for technical personnel to receive cash rewards for the transformation of scientific and technological achievements into positions? Do these rewards need to be included in the comprehensive income for annual tax settlement? 08

Answer:As of July 1, 2018, non-profit research and development institutions and higher education institutions, including national research institutions and universities, as well as private non-profit research institutions and universities, approved in accordance with the law, are required to provide cash rewards to scientific and technological personnel from the income derived from the transformation of scientific and technological achievements, as stipulated by the "Law of the People's Republic of China on Promoting the Transformation of Scientific and Technological Achievements."Eligible expenses can be reduced by 50% and counted as part of the monthly "wages and salary income" for scientific personnel, subject to individual income tax in accordance with the law. These expenses must be included in the comprehensive income for annual reconciliation.

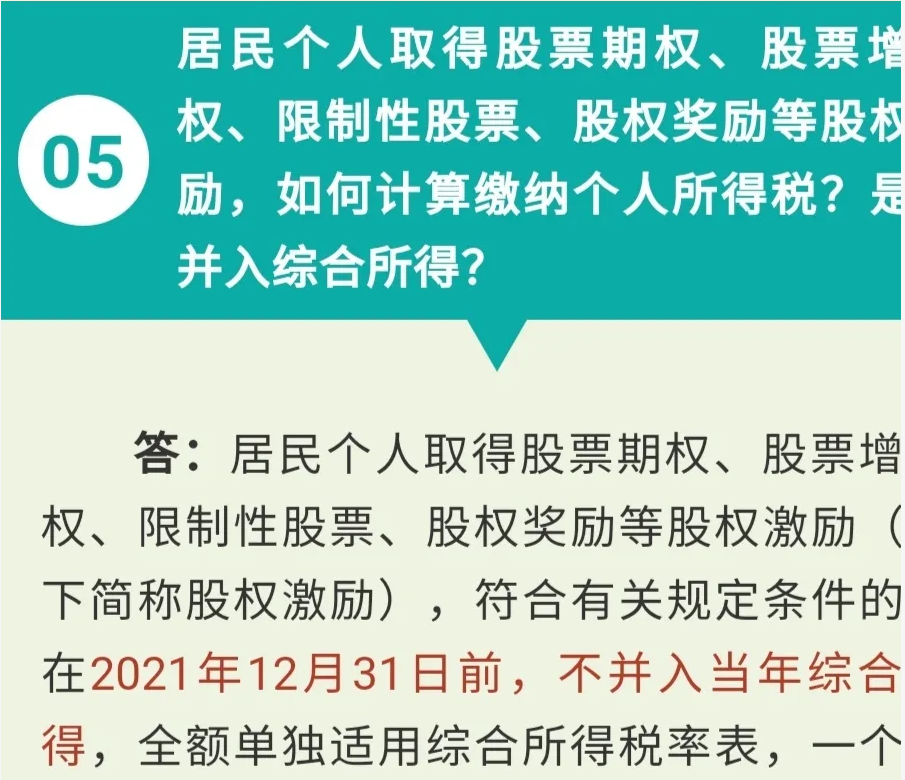

09How is the individual income tax calculated for equity awards given to technical personnel for the transformation of scientific and technological achievements by high-tech enterprises?

Answer:When an individual receives equity awards,Taxable amounts are calculated based on the "Income from Salaries and Wages" category. As of December 31, 2021, such amounts are not included in the comprehensive income of the same year.Taxation will be calculated using the comprehensive individual income tax rate schedule, with full application; the equity incentive policy for the period after January 1, 2022 will be specified separately.

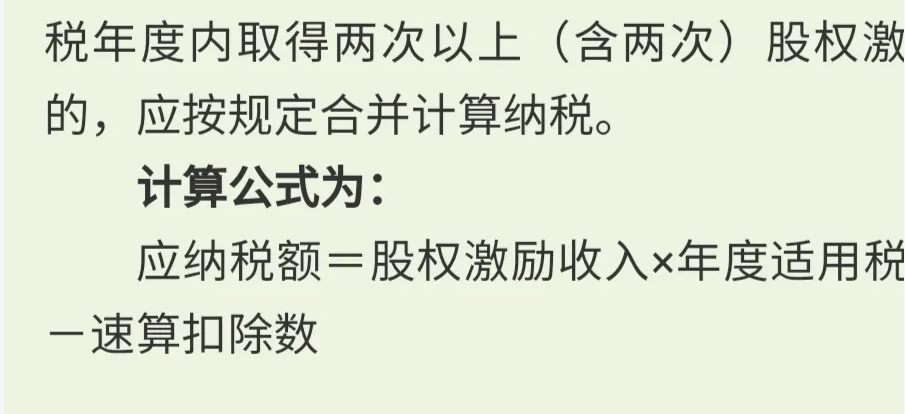

The calculation formula is:

Taxable Amount = Equity Incentive Income × Annual Applicable Tax Rate - Quick Deduction Amount

Individuals who receive two or more (including two) equity incentives within a tax year should be consolidated and taxed according to the aforementioned regulations.